Retail Inventory Method Calculator

What is the Retail Inventory Method?

The Retail Inventory Method is an accounting procedure used to estimate the value of a store’s inventory over time. It works by first taking the total retail value of all the products you have in your inventory, then subtracting the total amount of sales, then multiply that amount by the cost-to-retail ratio.

Downloadable Calculator

Download the calculator below that can simplify the process by allowing you to plug in your values and come up with your calculation that will save you time by not having to take a physical count of inventory.

<center><span id="hs-cta-wrapper-a83027e1-9823-4715-89db-36959813bf45" class="hs-cta-wrapper"><span id="hs-cta-a83027e1-9823-4715-89db-36959813bf45" class="hs-cta-node hs-cta-a83027e1-9823-4715-89db-36959813bf45"><a href="https://cta-redirect.hubspot.com/cta/redirect/3040938/a83027e1-9823-4715-89db-36959813bf45" target="_blank"><img id="hs-cta-img-a83027e1-9823-4715-89db-36959813bf45" class="hs-cta-img" src="https://no-cache.hubspot.com/cta/default/3040938/a83027e1-9823-4715-89db-36959813bf45.png" alt="DOWNLOAD CALCULATOR"></a></span><script src="https://js.hscta.net/cta/current.js" charset="utf-8"></script><script type="text/javascript">// <![CDATA[ hbspt.cta.load(3040938, 'a83027e1-9823-4715-89db-36959813bf45', {}); // ]]></script></span></center>

Retail businesses often sell large amounts of different smaller items that can make it hard to keep up with what you need to restock along with when.

For example, if you own a dollar store that sells an array of items that include deodorant, fidget spinners, dish soap, etc. It can be a hassle trying to make sure that you don’t run out of fidget spinners when you also have to worry about a plethora of other items. On the other hand, if you own a car dealership, you can easily keep records of how many of your 2018 Toyota Corollas you’ve sold by taking a physical count of inventory.

As you can see from these examples, Retail Inventory Method is crucial for retail businesses and restaurants that need a way to keep count of their individual items so that they aren’t in any sticky situations where a customer asks for something they don’t have.

You should be mindful that this method is heavily based on the relationship between the cost of the merchandise and its total price in retail. So although this method is useful, it’s methods make it inadequate for your year-end financial statements.

Running a retail business can get complicated, REALLY complicated. You have to manage employees, build their schedules, monitor your marketing strategies to understand what’s effective and what’s not, and you need to keep an accurate count of your business’s inventory to ensure you don’t run out of any products as well as ensuring you aren’t losing money on sales by calculating your cost-to-retail ratio correctly. The best way of making sure you don’t run out of products or lose any money is by mastering the retail inventory method.

Which is why I’ll be giving you a rundown on every aspect of the retail inventory method, along with a downloadable template that will allow you to easily plug in your own numbers so you’re able to get your own calculations.

Cost-to-Retail Ratio

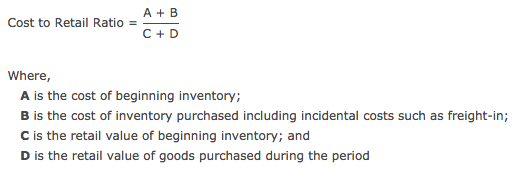

An important part of accurately using the Retail Inventory Method is understanding your business’s cost-to-retail ratio, which is the value of your merchandise that is found whilst using the retail inventory method.

Your cost-to-retail ratio is equal to the total amount of merchandise that’s available for your business to sell, divided by your retail value of items that are available for purchase.

Confused on what makes up the items that are available for purchase? They include any items that are available for sale at the beginning of the period along with any purchases of new inventory. Check out the example below to get a better idea of how it all works.

Say your Pizzeria has a beginning inventory with a cost of $10,000 and a retail value of $20,000. You then purchase $40,000 worth of new inventory that has a retail value of $80,000, its total cost of goods available for sale is $50,000 and the retail value of goods that are available for sale is $100,000. In this example, the Pizzeria’s cost-to-retail ratio is $50,000 divided by $100,000, which would be 50%.

Here is a visual display of the cost-to-retail ratio:

Cost Complement Ratio

The Cost Complement Ratio is a ratio in the form of a fraction where the numerator is the value of beginning inventory plus purchases during the tax year, and the denominator is the retail sales price of beginning inventory with the initial retail price of purchases added on. If you’re using the Retail Inventory Method to value inventories, you typically would not make adjustments to the denominator for markdowns.

Ending Inventory Cost

Another aspect of the Retail Inventory Method is the Ending Inventory cost which is a popular financial figure for measuring the final value of goods available for sale at the end of the accounting period. Although the number of units in ending inventory aren’t affected at the end of an accounting period, the dollar value of ending inventory is affected by whichever inventory valuation method is chosen.

In order to calculate the cost of ending inventory, follow the steps below:

1. Calculate the cost-to-retail percentage, where the formula is cost divided by retail price.

2. Calculate the cost of goods available for sale, where the formula is the cost of beginning inventory plus cost of purchases.

3. Calculate the cost of sales during the period, for which the formula is Sales times the cost-to-retail percentage.

4. Calculate ending inventory, for which the formula is Cost of goods available for sale minus Cost of sales during the period.

For example, say you own a company that sells coffee roasters for about $200, while you’re paying $140 per roaster. This would equal out to a cost-to-retail percentage of 70%. Your company’s beginning inventory has a cost of $1,000,000, you spent $1,800,000 for purchases during the month and sales of $2,400,000. The calculation of its ending inventory would look like this:

Drawbacks of the Retail Inventory Method

Not that we’ve gone through the components that make up the retail inventory method, it’s time that you understand the handful of cautions and drawbacks that come with the formula.

The Retail Inventory Method is only an estimate and the results won’t be as accurate as taking a physical count of inventory.

It only works if you have consistent markup across all of your products sold.

This method assumes that the historical basis for the markup percentage will continue into the current period. If a markup was different due to it being the Holiday season, then the results you get from the formula can be inaccurate.

Retail Inventory Method doesn’t work if an acquisition has been made and the one that acquired it holds large amounts of inventory at a significantly different markup percentage from the rate used by the acquirer.

Gross Profit Method

We can’t have an entire piece on Retail Inventory Method without touching on the other method of calculating the value of your inventory, Gross Profit Method. This is a technique used for estimating your store’s amount of ending inventory and can be used for your monthly financial statements when you’re unable to do a physical count because it’s too time-consuming due to the number of items in your inventory. Also, it’s often used to estimate the number of missing inventory that was caused by theft or some other situation.

It works by first finding your business’s gross profit margin. For example, if your supermarket buys its produce for 70 cents then sells the produce for $1.00, you would have a gross profit of 30 cents. 30 cents divided by the selling price of $1.00 equals out to be a gross profit margin of 30% of sales, which also means that your supermarket’s cost of goods sold is 70% of sales.

With the help of the retail inventory method, you’ll be able to save a ton of time & effort on figuring out the value of your stores’ inventory. Make sure to download the calculator attached to this template to make it easier on yourself and your employees.

Speaking of making it easier on your employees, what are you using to create your employee schedules? If you’re still using Excel or pen & paper, then you’re wasting hours each week of your managers’ time on a task that you could be automating. Along with that, your managers are left with much less time to focus on whats most important, which is figuring out how to make your business more profitable. To see for yourself how a platform like Deputy can strengthen your business, click on the link below to begin your free trial today!

<center><span id="hs-cta-wrapper-39f681b8-1b56-4081-bb18-1b80e3fc6617" class="hs-cta-wrapper"><span id="hs-cta-39f681b8-1b56-4081-bb18-1b80e3fc6617" class="hs-cta-node hs-cta-39f681b8-1b56-4081-bb18-1b80e3fc6617"><a href="https://cta-redirect.hubspot.com/cta/redirect/3040938/39f681b8-1b56-4081-bb18-1b80e3fc6617" target="_blank"><img id="hs-cta-img-39f681b8-1b56-4081-bb18-1b80e3fc6617" class="hs-cta-img" style="border-width: 0px;" src="https://no-cache.hubspot.com/cta/default/3040938/39f681b8-1b56-4081-bb18-1b80e3fc6617.png" alt="START FREE TRIAL"></a></span><script src="https://js.hscta.net/cta/current.js" charset="utf-8"></script><script type="text/javascript">// <![CDATA[ hbspt.cta.load(3040938, '39f681b8-1b56-4081-bb18-1b80e3fc6617', {}); // ]]></script></span></center>