Scheduling software

for small and medium

businesses

Unlock an easier way to schedule staff and get the business insights you need to grow.

TRUSTED BY 390,000+ WORKPLACES ACROSS THE GLOBE

“Staff can easily view their schedules on their phones and receive and confirm shifts, and without me having to get involved and find someone to take their shift.”

Chris Byrne, general manager, Boxpark

Your go-to platform

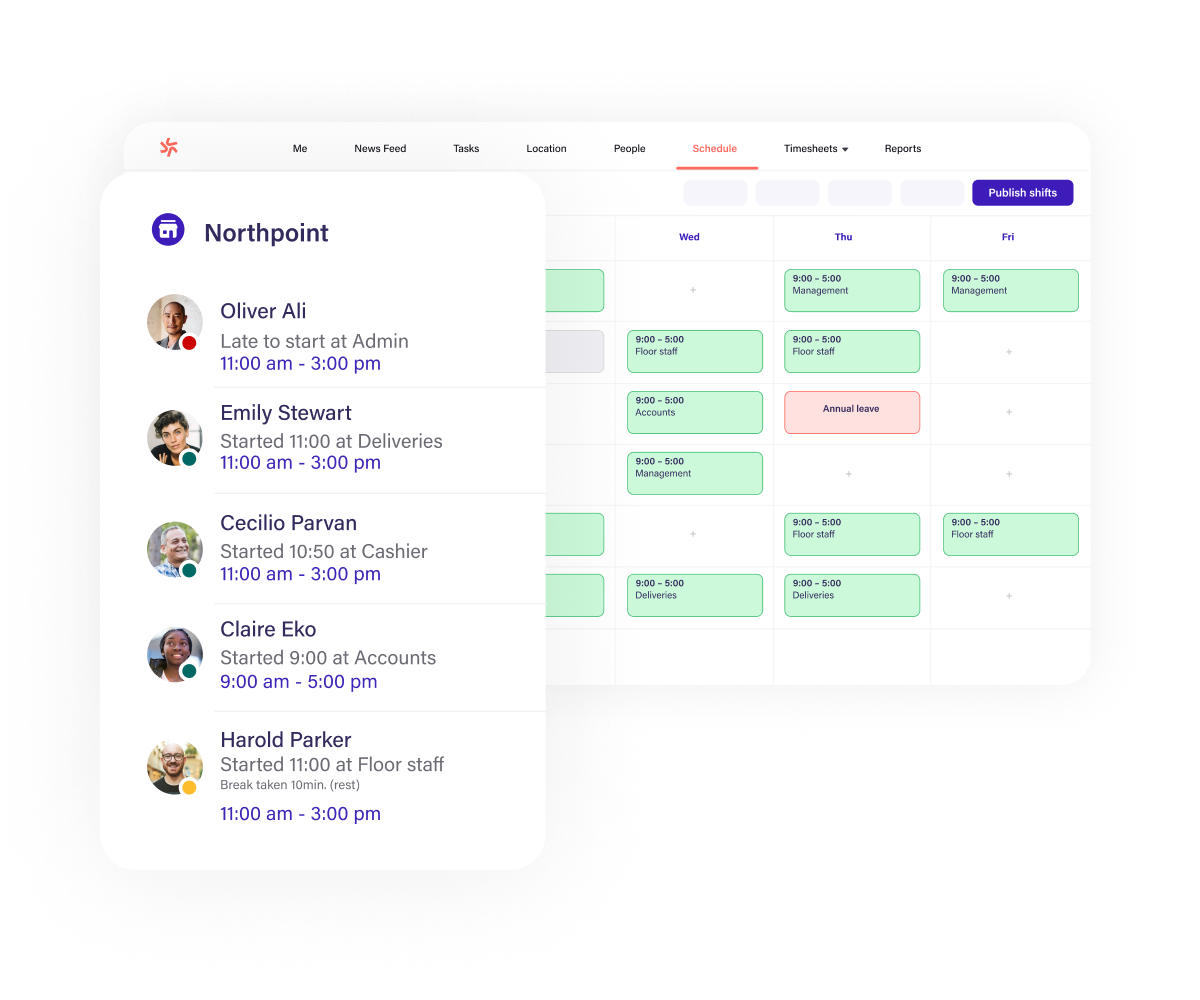

See everything in one place

Bring all your staff and key data together in one place that’s easy on the eyes. Keep track of staff availability, time off, hours worked, and wage costs without chaotic spreadsheets.

“Staff can easily view their schedules on their phones and receive and confirm shifts, and without me having to get involved and find someone to take their shift.”

Chris Byrne, general manager, Boxpark

“We now have a single source of truth for our schedules across all our European hotels and automated scheduling through templates and shift swaps.”

Matthew Bell, Operations Director, CitizenM

Efficient rotas

Simplify team scheduling

Create and share work rotas in minutes. Keep your team under budget. And always have the right number of staff on hand when your customers need them most.

“We now have a single source of truth for our schedules across all our European hotels and automated scheduling through templates and shift swaps.”

Matthew Bell, Operations Director, CitizenM

"Now, much of the day-to-day running of the business — from scheduling to holiday management to approving timesheets— is done directly from the Deputy app."

Sarah Aoki, Business Owner, Perfect Cleaning Solutions

Smart mobile app

Manage changes on the go

Approve shift swaps with one tap on mobile. Instantly find last-minute replacements when staff call in sick. And adjust rotas to meet changes in customer demand.

"Now, much of the day-to-day running of the business — from scheduling to holiday management to approving timesheets— is done directly from the Deputy app."

Sarah Aoki, Business Owner, Perfect Cleaning Solutions

"Management can assess the real-time costs of shifts, approve shifts and make journal entries against each job."

Rodney Jackson, Founder and Director, DallasAir

Team visibility

Track time and key insights

Get a clear picture of employee time, attendance, breaks, and overtime. Feel confident that everyone is paid for their exact hours.

"Management can assess the real-time costs of shifts, approve shifts and make journal entries against each job."

Rodney Jackson, Founder and Director, DallasAir

Take Deputy for a spin today

Seamlessly connect with your other systems

Deputy integrates with leading payroll, POS, and HR systems and gives you a smooth experience from day one.

What makes Deputy stand out?

The short answer is, our software is the easiest way to run thriving teams — and it's simple to pick up. Follow the links below for the bigger picture.

Frequently asked questions

- What is scheduling software?

Scheduling software is a kind of business software used by small and medium-sized enterprises to plan staffing rotas, holiday requests, shift patterns and payroll. Rather than using whiteboards or spreadsheets to plan rotas, using a specialised app makes planning shifts much more efficient and eliminates errors.

You can share rotas with staff via an app, email or text. Medium and small business scheduling software also includes many other features to help with people planning, including things like shift swapping, holiday requests or organising sick leave replacement.

- Why is Deputy the best scheduling app for small businesses?

Deputy was built by small business owners just like you who wanted to plan rotas more effectively. We designed our employee scheduling software for small businesses to include everything managers and business owners need to plan shifts, monitor staff costs, allocate tasks and more. That gives you more time to focus on the things that really matter.

Since launching in 2008, we’ve helped thousands of small businesses in the UK and worldwide to save time and money with fast, efficient and productive scheduling tools that also connect to their preferred payroll systems. And Deputy does more than ‘just’ rota planning. We’ve built powerful HR tools that mean you attract and retain the best staff, improve employee onboarding processes, and can use staff engagement and feedback tools that help boost morale.